Why are auto insurance rates continuing to climb?

Like any business, companies need to sustain higher gross than expenses in order to stay viable. Auto insurance is no unlike ; companies make money from the premiums customers pay, but lose money when they fulfill their obligation to pay for damages. They besides have a host of engage expenses to pay, including agent compensation and advertising .

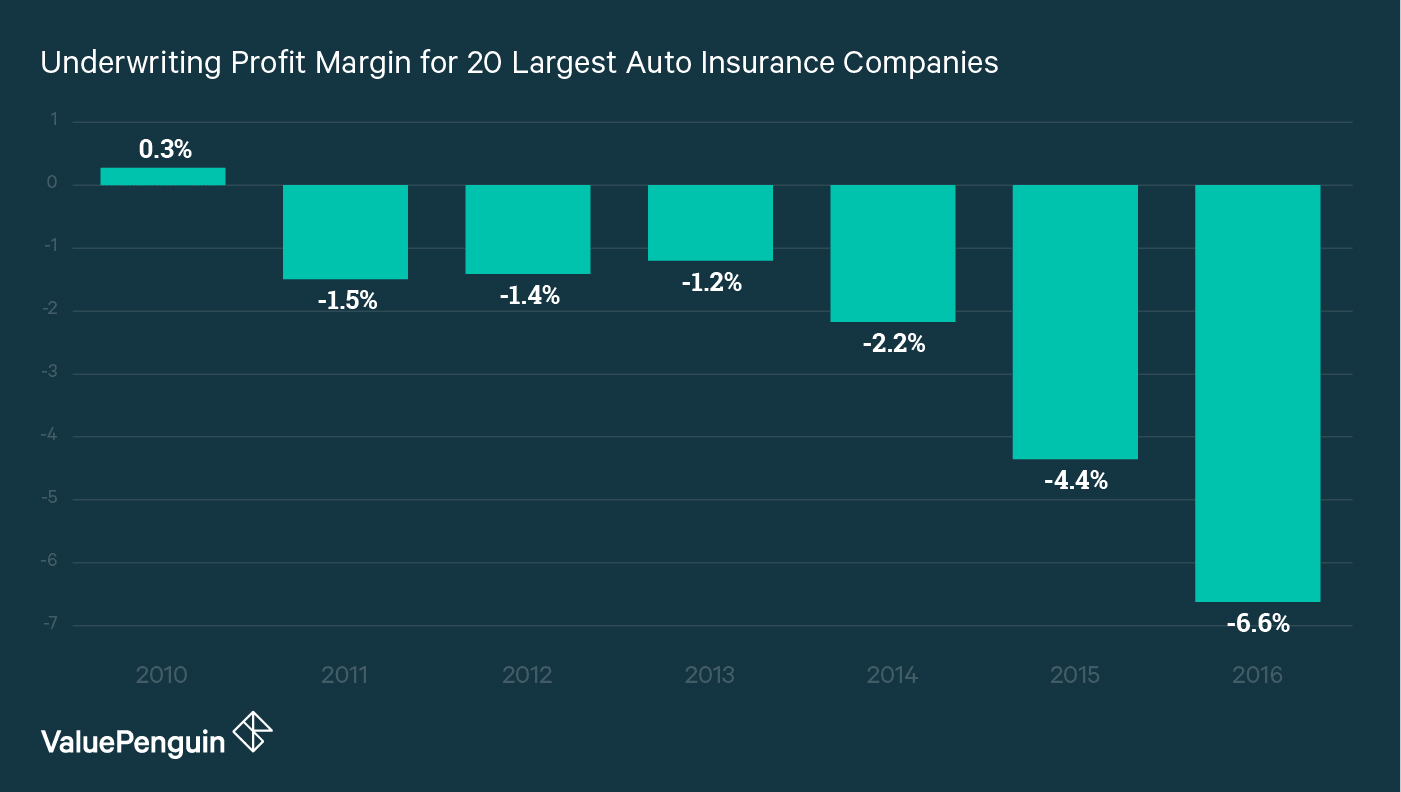

The proportion of expenses to tax income is called the “ blend loss proportion, ” and whenever it is above 100 %, the company loses more money than it is earning. In 2016, entirely two of the crown 10 car policy companies in the country had combined ratios below 100 % — and merely scantily .

|

Company |

Premiums written ($B) |

Premium increase since 2015 |

Combined loss ratio 2016 |

|---|---|---|---|

| State Farm | 39.19 | 7.25% | 117% |

| Berkshire Hathaway | 25.13 | 11.94% | 99% |

| Allstate | 20.81 | 3.88% | 100% |

| Progressive | 19.63 | 12.08% | 96% |

| USAA | 11.69 | 10.69% | 107% |

| Liberty Mutual | 10.76 | 8.18% | 109% |

| Farmers | 10.30 | 3.19% | 111% |

| Nationwide | 7.64 | 2.30% | 114% |

| American Family | 4.01 | 8.43% | 109% |

| Travelers | 3.90 | 15.38% | 105% |

Berkshire Hathaway is the rear company of Geico. generator : SNL Financial

indeed, even if you have never been in an accident, your rates may hush go up because insurers are trying to bring their ratios below 100 %. Imagine a major drought destroying region of a farm ‘s crops, and then the grow charging more for the crops that survived in decree to make up for the ones they lost. It ’ s the lapp principle with your car insurance company. In 2010, the situation was the exact inverse. only two of the top 10 companies were operating with combined loss ratios over 100 %. The modal unite loss proportion was 99.7 % in 2010, compared to 107.1 % in 2016. The average combined proportion has climbed year after year, and as a leave, car insurance rates have gone up an average 20 % across the state .

unfortunately, the rate hikes have not been effective at closing the opening between profit and loss. All the insurers in the table increased their written premium revenues in 2016 ( largely ascribable to pace hikes ), however they silent ( with the exception of Allstate ) ran higher combine loss ratios. The current tendency indicates that the companies are getting further from turning underwriting profits again. even after three solid years of increases, the companies are not just still losing money — they ‘re losing an even greater measure .

Why are auto insurance companies losing so much money?

In their fiscal statements, Geico, Progressive and Allstate didn ’ thyroxine hesitate to blame bad weather as a significant informant of their losses. In its fiscal instruction, Progressive said catastrophe losses as of the end of the third quarter were “ $ 121.0 million greater than in the same period survive class. ” They attributed $ 85 million to Hurricane Matthew entirely .

Comprehensive claims, which may result from catastrophic weather, can average upwards of $1,700 per claim, according to the Insurance Information Institute, so those figures make sense given the number of people that could be affected by a hurricane. The floods in Louisiana, which were besides explicitly cited in fiscal statements, besides ended up costing insurers millions of dollars .

But it ’ s not just the weather. Drivers are crashing more than they have in about a decade. The National Safety Council, a nonprofit organization that advocates for safety, found that black centrifugal accidents went up 6 % from 2015 to 2016, for a total of 40,200 fatalities — the most since 2007. The National Highway Traffic Safety Administration blames distracted driving due to texting as a large beginning for the increase in fatalities .

More disasters and more accidents lead to more claims, therefore more payouts from insurers. In 2017, the phone number of households with at least one car indemnity claim in the past three years increased by 3,869,969 compared to 2014. In 2017, 22.2 % of households had at least one car insurance call, while 20.5 % had one in 2014. Nielsen, which compiled the data, projects that by 2022, 22.5 % of households will have at least one car claim .

How much will car insurance cost in the future?

It ’ s unmanageable to pinpoint future car policy price with certainty. What you could pay for car indemnity in the near future is probably more than what you are paying now — even if you have a clean drive record.

The trends that are causing more accidents — lower flatulence prices leading to more drivers on the roads, drivers distracted by texting and so on — are not likely to abate. other important factors like hard weather are unmanageable to predict .

The Colorado State University Tropical Weather & Climate Research has forecasted this hurricane season to be below average in terms of the number of named storms. They can not predict however how many of those storms will hit the U.S. So, even if hurricane season is under modal in terms of the number of storms, if the number of storms that hits the U.S. is above average, the property damage costs would be enormous and an even heavier effect on insurers .

On the other hand, if the weather turns out to be favorable, or another factor discourages people from driving, insurers may start to see better margins and feel no indigence to raise rates further. Again, it is all notional and lone time can tell .