Insurers by and large raise rates when the gap between what customers pay and what is paid out starts to shrink, which is normally attributed to fleshy losses caused by frequent and austere claims .

not only are insurance claim payouts in Michigan among the highest in the country, but they besides primarily root from no-fault/personal injury protection ( PIP ) claims. If not for Michigan ‘s huge PIP payouts ( even when compared to other no-fault states ), it can be argued that the state ‘s car insurance rates would not be angstrom high as they are .

The rise in Michigan’s auto insurance rates slowed significantly since 2017

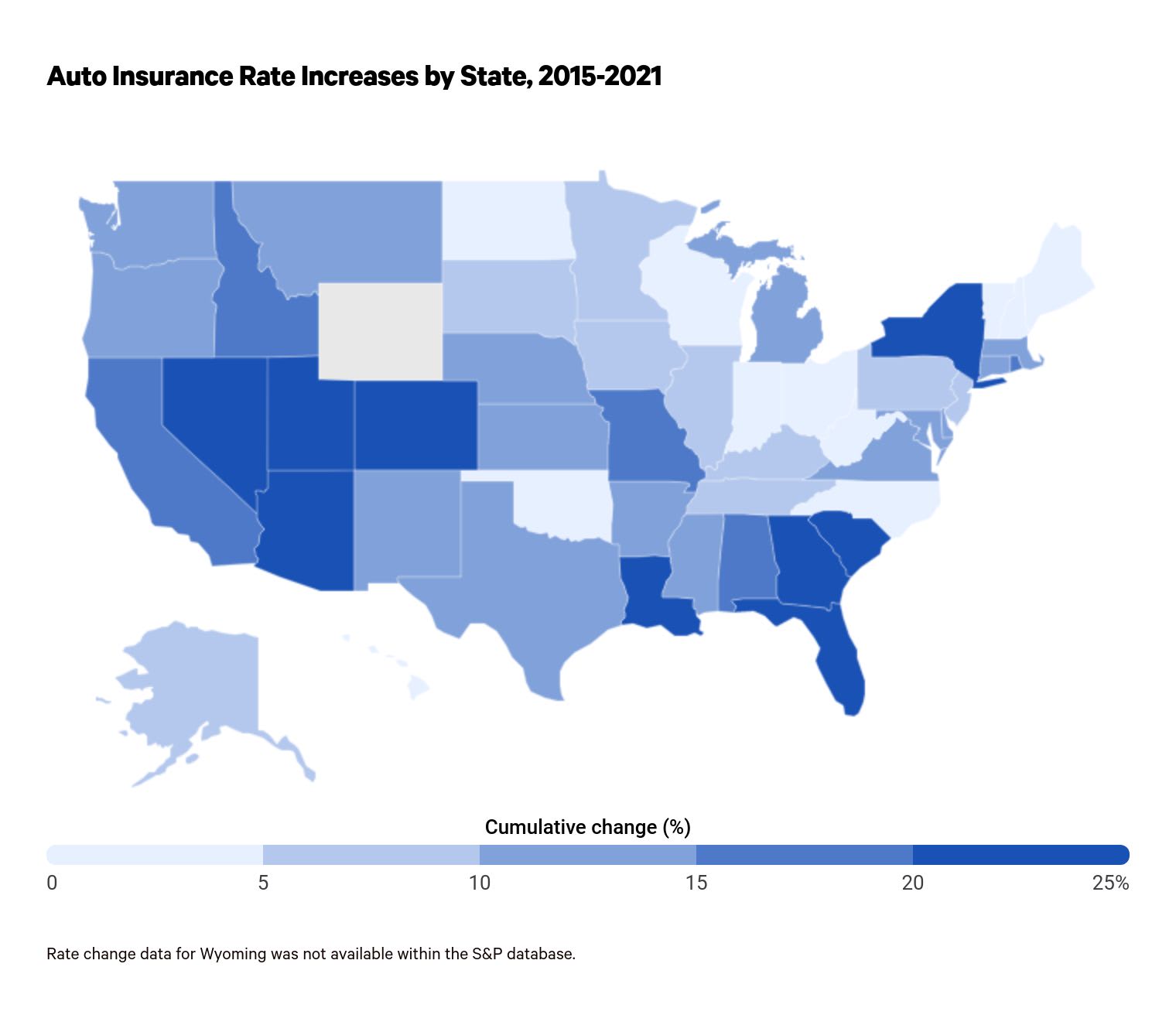

The largest insurance companies in Michigan have raised cable car policy rates by an average of 13% since 2015. That ‘s a significant slowdown after a 47 % jumpstart from 2011 to 2017.

Why do some states experience higher rates than others ? There are numerous reasons, but an insurance company ‘s profits on policies, often called loss ratios, play a big part. If companies see constrict or negative profit margins in a given market, they tend to raise rates there .

In Michigan, those ratios have dipped dramatically in recent years, from 136 % in 2011 to 82 % in 2020. This likely explains the slow in the rise of prices .

Most auto insurance losses in Michigan come from no-fault losses

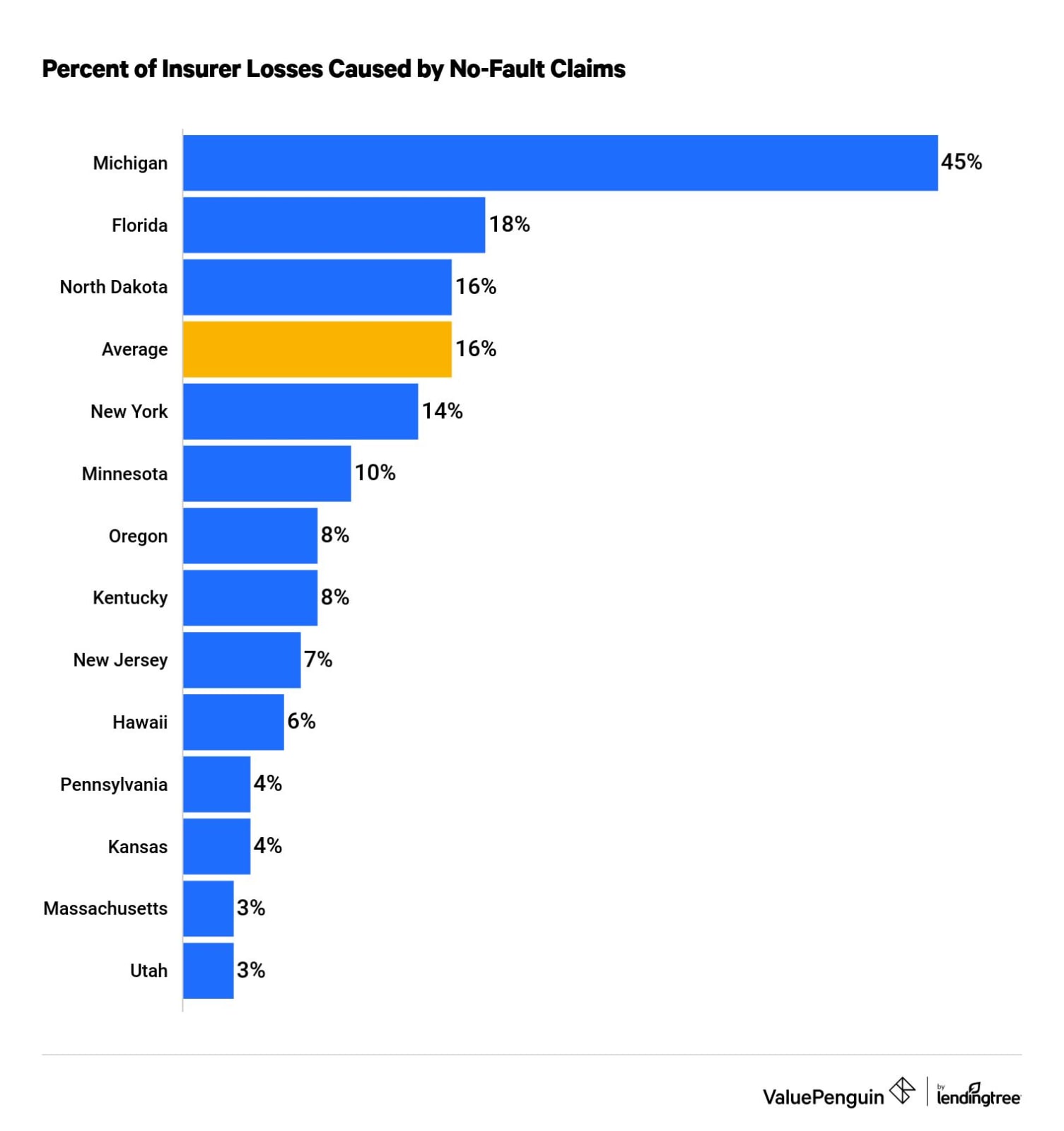

When we looked into the causes of the high combined policy payouts in Michigan, we found that a major fortune of those losses stemmed from no-fault or PIP claims. Over the past decade, 45 % of all car indemnity losses in Michigan were no-fault losses. That ‘s significantly more than the 16 % of average sum losses that no-fault losses account for across the U.S .

Why are Michigan ‘s losses sol much greater than everywhere else ? It is probable driven by the fact that Michigan PIP has a minimum specify of $ 250,000. Higher PIP limits means higher payouts and thus higher losses .

No-fault losses likely driving force behind decline of Michigan rate increases

The slow of Michigan ‘s car insurance rate increases runs alongside some stability in terms of no-fault losses disappearing. From 2011 through the middle of 2016, that character of policy cost Michigan companies 66 % more than it was taking in .

In recent years, however, whether by increasing prices or fewer claims, those numbers have flipped. The combine loss ratios of those policies in Michigan are no longer more than 100 %, meaning they ‘re no longer losing money .

|

Year |

No-fault CLR in previous year |

Rate increase |

|---|---|---|

| 2016 | 119% | 4% |

| 2017* | 136% | 6% |

| 2018 | 122% | 3% |

| 2019 | 126% | 3% |

| 2020 | 76% | -4% |

| 2021 | 82% | 1% |

The other components of car indemnity — liability, collision and comprehensive examination coverage — remained much more manageable for Michigan insurers. The combine loss proportion due to liability claims ( those filed through bodily wound liability or property damage liability ) in 2020 was 76.8 % while the loss ratio from physical damage claims ( collision and comprehensive ) was 68.9 % .

Why is car insurance so expensive in Michigan?

cable car insurance is expensive in Michigan because the state has some of the highest minimum policy requirements of any state. That means higher prices for more compulsory coverage .

Michigan drivers pay an average of $7,161 per year for full-coverage indemnity. That ‘s 270 % more than the national average and close to double the following most expensive country .

Michigan has some of the highest minimum-liability coverage requirements in the country and requires most drivers to carry at least $ 250,000 in PIP coverage .

|

Coverage |

Limit |

|---|---|

| Bodily injury liability | $50,000 per person/$100,000 per accident |

| Personal injury protection | $250,000 |

| Property damage liability | $25,000 per accident |

| Uninsured/underinsured motorist bodily injury | $50,000 per person/$100,000 per accident |

| Comprehensive and collision | $500 deductible |

additionally, the state of matter has a high percentage of uninsured drivers, more than 25 %, which besides raises insurance rates .

Methodology

We obtained fiscal information on no-fault loss ratios and rate increases for Michigan car insurers in all states through the S & P Market Intelligence Tool. Data on uninsured drivers was from the Insurance Research Council .