Depending on the insurance company, minimum-coverage car insurance can vary by more than $ 5,000. That shows why shopping around can help you save money .

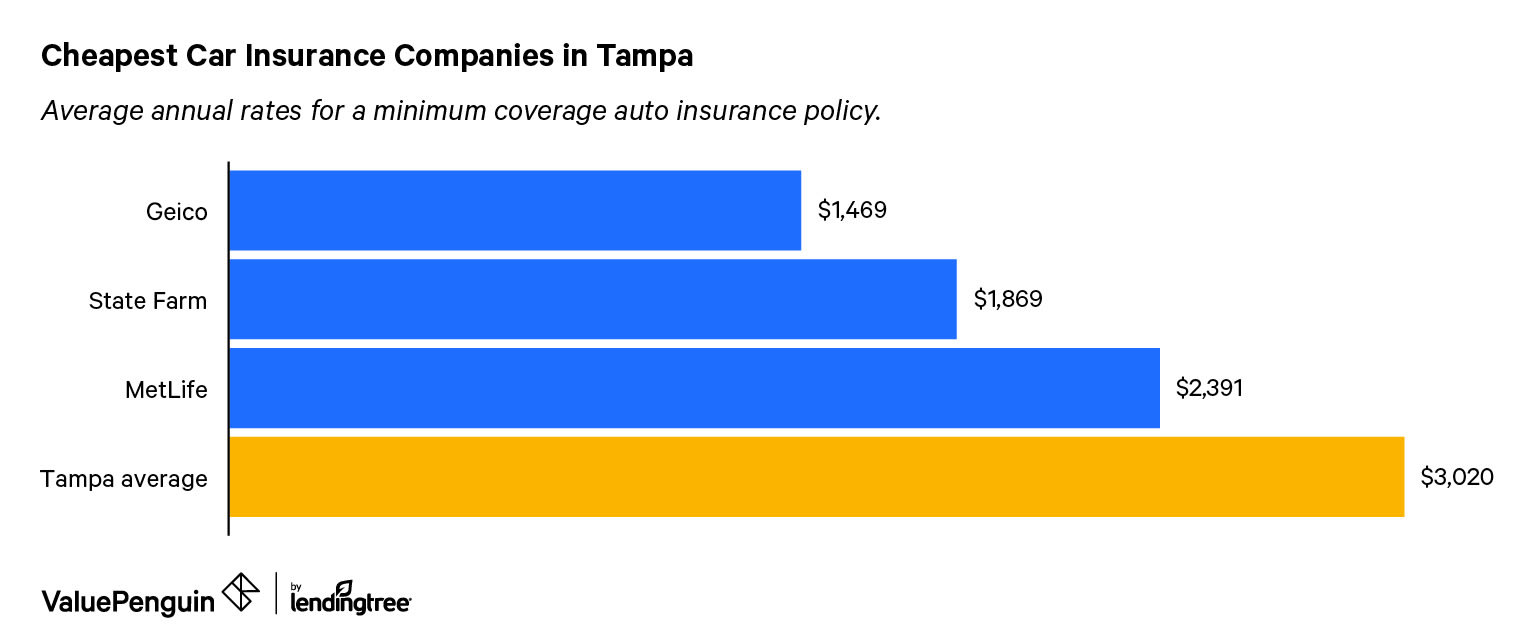

Who has the cheapest insurance rates in Tampa? Geico

Geico and State Farm offered the most low-cost rates for a minimum-liability policy in Florida. On average, these companies charge less than $ 2,000 per year. A minimum-coverage policy comes with the lowest measure of coverage required by Florida law. policy costs tend to climb in densely populated areas. Tampa is the largest city in the Tampa Bay area and the third-most populated city in Florida, so it ‘s no surprise insurance rates are higher than the state average.

Find Cheap Auto Insurance Quotes in Tampa, FL

presently insured ? The minimum-liability policy is your cheapest option for coverage, but it might not be the best for your individual needs. Keep in mind that a minimum policy does not cover damage to your vehicle. If you get into an accident and hard damage your car, your insurance wo n’t cover the costs of the wrong .

Cheapest full-coverage policy for Tampa drivers? Geico

Geico with an average premium of $2,331 per year.

The Tampa insurance company with the cheapest full-coverage policy iswith an average premium of $ 2,331 per year. If you ‘re looking for an alternative, the second-cheapest option is State Farm, which costs $ 693 more than Geico on average .

|

Rank |

Company |

Annual premium |

|---|---|---|

| 1 | Geico | $2,331 |

| 2 | State Farm | $3,024 |

| 3 | Direct General | $3,983 |

| 4 | MetLife | $4,570 |

| 5 | Progressive | $5,289 |

| 6 | Allstate | $7,442 |

A full-coverage policy costs more than a minimum-liability policy but offers more protection. namely, it comes with comprehensive and collision coverage .

- Comprehensive coverage financially protects you from damage caused by events out of your control, known as “acts of God.” Those events may include natural disasters, theft, vandalism and fires.

- Collision coverage protects you from damage caused by driving into another vehicle or object. For example, if you crash into another car, drive into a ditch or flip your car over, collision coverage would pay to fix your car’s damage.

If your car is less than 10 years previous or worth more than $ 3,000, you ‘ll benefit the most from purchasing a full-coverage policy. But if your cable car is n’t worth much, then investing in a full-coverage policy might not be worth it. You could end up spending more on policy than your actual vehicle is worth .

Cheapest full coverage for young drivers? Geico

young drivers in Tampa will find the cheapest indemnity quotes with Geico, which has an average annual cost of $ 4,070 — slenderly cheaper than the city average .

|

Rank |

Company |

Annual rate |

|---|---|---|

| 1 | Geico | $4,070 |

| 2 | Direct General | $5,085 |

| 3 | State Farm | $5,334 |

| 4 | MetLife | $6,160 |

| 5 | Progressive | $9,751 |

| 6 | Allstate | $12,429 |

Age is one of the biggest factors that affects indemnity rates. Young people typically pay more for car policy, on average, than middle-aged drivers. adolescent drivers are the most likely to be involved in an accident out of any group, making them a risk to insure .

In fact, the average cost of full-coverage policy for young people is about doubly the monetary value for drivers in their 30s .

There are extra steps every driver, specially young ones, should take to mitigate insurance costs :

- Combine plans Rates for a combined or multicar insurance plan are more expensive than a single car or driver rate. However, a combined plan is less expensive than having two separate policies.

- Look for discounts Most insurers offer a menu of discounts to drivers. You can receive discounts for achieving good grades in school, attending a defensive driving course and installing anti-theft devices in your car.

- Gather quotes from more insurers. The difference between the cheapest and most expensive insurer for young Tampa drivers is more than $8,000. Research smaller insurers as well as widely known companies to see if they have affordable quotes.

Cheapest insurer for drivers with an accident history

Tampa drivers with an accident on their record should look at Geico, which offered us the best price for car insurance after an accident .

Drivers with a history of even a single accident know that it weighs heavily on policy costs. insurance premiums increase constantly after an accident. The companies that increased prices the least following an accident were :

- State Farm

- Geico

- Direct General

|

Rank |

Company |

Rate before accident |

Rate after accident |

Difference |

|---|---|---|---|---|

| 1 | State Farm | $3,024 | $3,599 | $575 |

| 2 | Geico | $2,331 | $3,365 | $1,034 |

| 3 | Direct General | $3,983 | $5,453 | $1,470 |

| 4 | Progressive | $5,289 | $7,481 | $2,192 |

| 5 | MetLife | $4,570 | $7,607 | $3,037 |

| 6 | Allstate | $7,442 | $10,707 | $3,265 |

Accidents may cause your premiums to increase and disqualify you from good and safe driver discounts. It ‘s authoritative that when you ask around for quotes, you besides ask how an accident will impact your rates .

Best auto insurers in Tampa by customer service

When searching for the best insurance company for your needs, it ‘s crucial to consider both the price and military service quality. The companies with the best serve, measured by the frequency of customer complaints, are Amica, Florida Farm Bureau, Southern-Owners and Progressive .

Read our wide breakdown of the best car insurers in Florida for more information .

|

Rank |

Company |

Complaint Index |

|---|---|---|

| 1 | Amica | 0.06 |

| 2 | Florida Farm Bureau | 0.07 |

| 3 | Southern-Owners | 0.10 |

| 4 | Progressive | 0.10 |

| 5 | Safeco | 0.11 |

Show All Rows

Car insurance costs across Tampa ZIP codes and neighborhoods

In Tampa, your vicinity will impact your annual car insurance rates. If you live in New Tampa, the cheapest area of Tampa, you ‘re paying $ 757 less than your supporter or colleague in Northwest Tampa, a tourist concentrate and one of the most expensive areas of Tampa .

|

ZIP code |

Neighborhood |

Average cost |

|---|---|---|

| 33602 | Downtown | $3,323 |

| 33603 | South Seminole Heights | $3,370 |

| 33604 | Old Seminole Heights | $3,304 |

| 33605 | Palmetto Beach/Ybor City | $3,292 |

| 33606 | David Islands/Hyde Park | $3,237 |

Show All Rows

Auto theft statistics in Tampa, Florida.

Tampa has the lowest vehicle larceny rate out of the eight largest cities in Florida. The city ‘s car larceny rate is about one-half that of Jacksonville, Florida ‘s most populate city .

|

City |

Population |

Car thefts |

Thefts per 100,000 people |

|---|---|---|---|

| Fort Lauderdale | 182,150 | 426 | 233.9 |

| Orlando | 286,679 | 602 | 210.0 |

| Tallahassee | 192,443 | 336 | 174.6 |

| Miami | 473,047 | 815 | 172.3 |

| St. Petersburg | 265,942 | 377 | 141.8 |

Show All Rows

Car insurance companies in Tampa, Florida.

The 11 biggest players in the Florida car policy grocery store write about 82 % of all premiums. Each large insurance company varies in terms of average price, number of policy offerings and serve timbre, among early factors .

If you ‘re debating between whether to receive insurance from a boastfully company or a small party, you should keep in mind the benefits and disadvantages of each, a well as your own needs. large insurers have a greater offer of discounts, policies and handiness but lack the individualized service approach that small insurers possess .

|

Rank |

Insurers |

Direct premiums written |

Percent of direct premiums |

|---|---|---|---|

| 1 | Geico | 5,492,413 | 22.67% |

| 2 | Progressive | 5,001,524 | 20.64% |

| 3 | State Farm | 2,903,833 | 11.98% |

| 4 | Allstate Corp. | 1,999,192 | 8.25% |

| 5 | Liberty Mutual | 618,341 | 2.55% |

Show All Rows

Auto insurance in Tampa: Minimum insurance requirement in Florida

car indemnity coverage requirements are set by the state of matter of Florida. In decree to legally drive in Tampa, all drivers must meet the follow requirements :

indemnity in Florida is generally more expensive than in other states, so you might be tempted to buy the minimum total of coverage. however, a minimum-liability policy might not be enough to protect you financially if you ‘re involved in an expensive accident. Drivers with expensive or modern cars should consider a higher coverage limit or extra protection .

No-fault state

No-fault policy covers your medical costs following an accident, regardless of who was at fault. Drivers are n’t allowed to file claims or seek litigation against another driver after an accident .

The type of no-fault coverage required in Florida is personal injury auspices ( PIP ), which financially covers medical bills for you and your passengers .

Florida’s financial responsibility law: SR-22 and FR-44 policies

If you are convicted of driving under the determine or without policy, you are required to hold extra coverage and higher coverage limits under Florida ‘s fiscal province law in the kind of SR-22 or FR-44 policy .

SR-22 insurance requirements

Drivers who do n’t have insurance or have besides many points on their drive records are seen as high risk. These drivers may need to ask their insurance company to file an SR-22 second. The mannequin acts as proof that you meet the following policy coverage requirements :

- Bodily injury liability: $10,000 per person/$20,000 per accident

- Property damage liability: $10,000 per accident

How long you must have an SR-22 sanction will need to be verified with your local Department of Motor Vehicles ( DMV ). In most cases, you will need to have an SR-22 on file for at least three years in Florida .

FR-44 insurance requirements

FR-44 is generally required for drivers found guilty of driving under the influence ( a DUI ) or driving while intoxicated ( a DWI ). due to the earnestness of these offenses, drivers filing for FR-44 will need to pay for importantly higher coverage limits .

- Bodily injury liability: $100,000 per person/$300,000 per accident

- Property damage liability: $50,000 per accident

Methodology

ValuePenguin examined data from six Tampa indemnity companies. Unless specified differently, our sample distribution driver was an unmarried 30-year-old man who owned a 2015 Honda Civic EX. The driver was looking to purchase a minimum car insurance policy and had a hapless credit rating history .

In instances where our Tampa driver was opting for a full-coverage policy, the following limits were implemented :

|

Coverage type |

Study limits |

|---|---|

| Bodily liability | $50,000 per person/$100,000 per accident |

| Property damage | $25,000 per accident |

| Uninsured/underinsured motorist bodily injury | $50,000 per person/$100,000 per accident |

| Comprehensive and collision | $500 deductible |

ValuePenguin ‘s psychoanalysis used indemnity rate data from Quadrant Information Services. These rates were publicly sourced from insurance company filings and should be used for relative purposes entirely — your quotes may be different .